The 2026 Integrated System Plan is admirably precise about where the grid should arrive, and quiet on whether it can get there. On its own figures, it cannot.

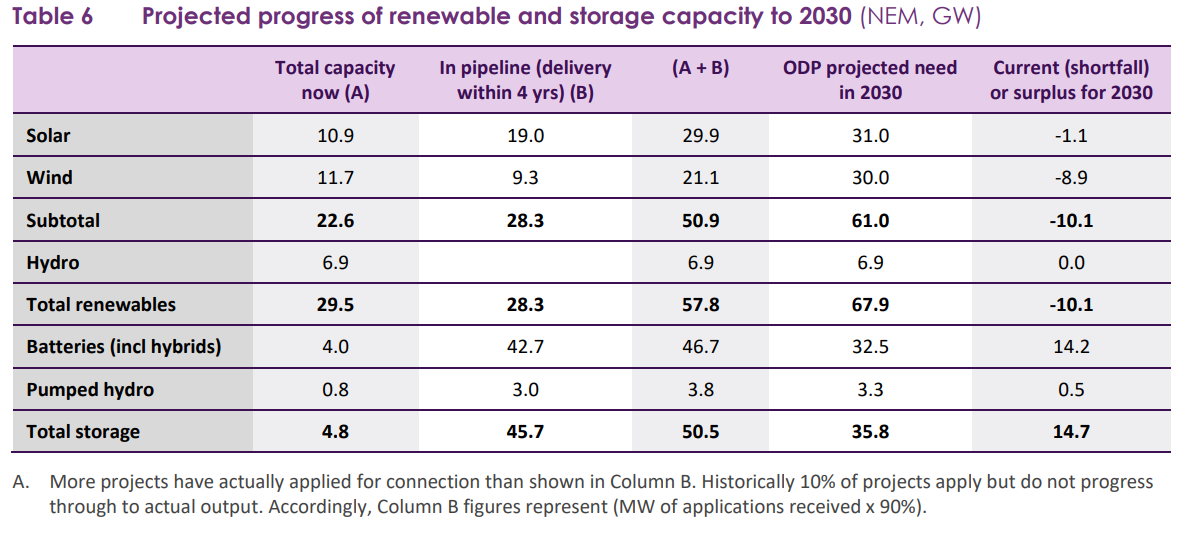

The Australian Energy Market Operator published the final 2026 Integrated System Plan on 24 June. It is a thorough piece of work, which is summarised by a single table reproduced below. To meet the 2030 target the grid requires about 30 gigawatts of wind. It has 11.7 today, with a further 9.3 in the connection pipeline, which leaves it short by 8.9. Storage has gone the other way: some 45 gigawatts of batteries are in development against a need of roughly 33. The market is building a great deal of the one thing and not nearly enough of the other.

Exhibit 1. Projected progress of renewable and storage capacity to 2030 (NEM, GW). Source: AEMO 2026 Integrated System Plan

This is not a failure of effort, and it is not, on any sensible reading, a failure of engineering. It is a question of what can be financed, approved and connected. A battery makes its money trading the market and selling firming services, and it can reach financial close without a single customer promising to buy its output (although it’s better if they do). A wind farm earns nothing until someone signs a contract lasting fifteen years, and at present almost no one will. Capital has behaved as anyone might have predicted, the more so as wind construction costs have risen. It has gone where the revenue is contracted and kept away from where it is not. The pipeline is a reliable guide to what lenders will support and a poor one to what the system needs.

AEMO is not unaware of this. The Plan is a least-cost optimisation, and an optimisation takes the delivery of its inputs on trust. What candour there is sits in the scenario placed beside the main case – constrained delivery. Under constrained delivery, in which projects run late and cost more, renewables reach 75 per cent of supply by 2030 rather than the 82 the law requires, and the overrun exceeds the 30 per cent the scenario has already granted itself. To hold the central path, wind must be built at something above 2 gigawatts a year against a current rate nearer 0.3. Nothing in the past twelve months suggests the larger number is within reach.

The Plan is therefore clear about the destination and silent about the road. That is a perfectly respectable thing for the ISP as it was never intended to be the central energy transition plan. But it is a hazardous thing for a country to mistake for the ISP as a plan of action. That everyone in the sector quietly concedes it will not be built on time is not an excuse. It is the admission. One cannot manage what one has declined to schedule, and at present the build is not being scheduled by anyone. The distance between the model and the means of achieving it is now wide enough to lose a legislated target inside.

A delivery plan, as opposed to a forecast, would attend to three matters the ISP is content to leave to others.

The first is to reduce the quantity that must be built at all. The genuinely encouraging number in the 2026 Plan is consumer energy. Rooftop solar now generates more than grid-scale solar, wind or hydro, and on one afternoon last October households, their batteries and a little managed demand met more than three-fifths of the entire market. Coordinated, that fleet is firm capacity, and every megawatt of it is a megawatt of wind and transmission the system is spared. The trouble is that it is arriving faster than anyone is organising it, and coordination is running well behind the previous plan. The remedies are unglamorous and thoroughly understood: common rules for aggregating household assets, putting in place consumer protections to encourage up-take of VPPs, time-of-use pricing as the default rather than a favour granted on request, and a distribution network mandated to operate the system rather than merely to maintain it. This is the cheapest capacity available, it commands public support, and it is the least likely of any measure to find itself before a planning tribunal. It is a sensible place to begin.

The second is to give the wind that must still be built a revenue it can bank. The Capacity Investment Scheme has named close to 11 gigawatts of wind, across 25 projects, as successful in its tenders. Unfortunately, only a handful have gone on to agree a contract, and three have reached financial close. The numbers are not a verdict on the scheme, which was built for a market in which projects carry some merchant risk, and storage has taken to it readily. They are a verdict on fit. A revenue collar leaves a wind project exposed in the places its lenders look first, and the lenders have looked, and declined. What wind wants is a creditworthy buyer for its output at a firm price, and another round of tenders will not produce one.

The remedy does not require a new institution or a further review. For wind, the Commonwealth should contract on a firm price: a power purchase agreement in the ordinary commercial form, written directly or through the ESEM it has already undertaken to build. The balance to be struck is between the lowest price that carries a project to financial close and the least cost to the taxpayer over the fifteen years that follow, and a firm price serves both ends of it. It gives the project the revenue certainty its lenders require, which is the whole of the present problem. And it caps the public liability more cleanly, because a collar underwrites the floor in full while returning only about half of whatever sits above the ceiling, whereas a firm price keeps all of the upside with whoever holds the contract.

That last point matters, because a firm-price contract can be sold, and the state need not hold it to term. It can write the contract now and pass it on as demand appears that is willing to assume it, and that demand is not imagined. Data centres are expected to account for close to a tenth of national electricity demand within the decade, and they are concentrated in New South Wales, which is where the new wind is supposed to go. Obliged to contract for new supply rather than lean on the existing system, they are the parties to whom the contracts can in time be handed, as in the end are the retailers that return to the market as coal leaves it. The public exposure is then counted in three or four years, not fifteen. It is less a subsidy than a bridge across the period before the buyers arrive.

The third is the most practical, and the least attended to: to move the projects that are ready through the system in the order the system needs them, not the order in which they happened to apply. Planning consent and grid connection both run, in effect, on the rank of the cab. Each application is dealt with as its turn arrives, so that a project which is financed, contracted and central to a renewable energy zone can sit behind one that is speculative or going nowhere. The queue is treated as inviolable. Prioritisation would order the pipeline by system need, location and readiness, and carry the projects that meet those tests to the front of both the planning and the connection process (an alternative approach, suggested in the US is auctions for connection slots). It would hold the assessing bodies to dates that bind, and it would run planning, connection and the transmission meant to serve them together rather than one after another. This is not a matter of choosing which projects live and which die; the queue still clears. It is a matter of the sequence in which it clears.

This approach does not lower the ambition of the plans. It does the opposite. The 82 per cent target should stand, and so should the wind beneath it. A target with no credible means of attainment costs more than a slightly later one that can be delivered, because the failure shows up first in prices and in reliability, and it is on those that public tolerance for the whole enterprise ultimately rests. Coal will still leave. Prices will still recover as it goes. The grid of the 2030s can be considerably more ambitious than the one now drawn. That ambition is purchased by assembling the means of delivery in this decade, not by the cheaper expedient of announcing a larger number.

The instruction to officials should not be to produce a better forecast. The forecast is sound enough. It is to build the plan the forecast has assumed all along: to organise the household fleet before next summer rather than the one after, to stand up the offtaker that gives wind a buyer, and to reorder the planning and connection queues so that the projects the system needs are not held behind the ones it does not. The 2026 Plan has discharged its function. It has told the government, in the government’s own figures, that the present course will fall short. What follows is a matter for decision, and the time in which to take that decision well is not generous.

Cyan Ventures advises on, and invests in, clean-energy projects at the development stage, including the financing gap described above. The case is put on its merits.